Kenyan Tourism-Focused Venture Studio Purple Elephant Ventures Raises Additional $500,000

Nairobi-based Purple Elephant Ventures (PEV), a startup studio focused on tourism, has secured an extra $500,000 to boost its seed funding round to $5 million.

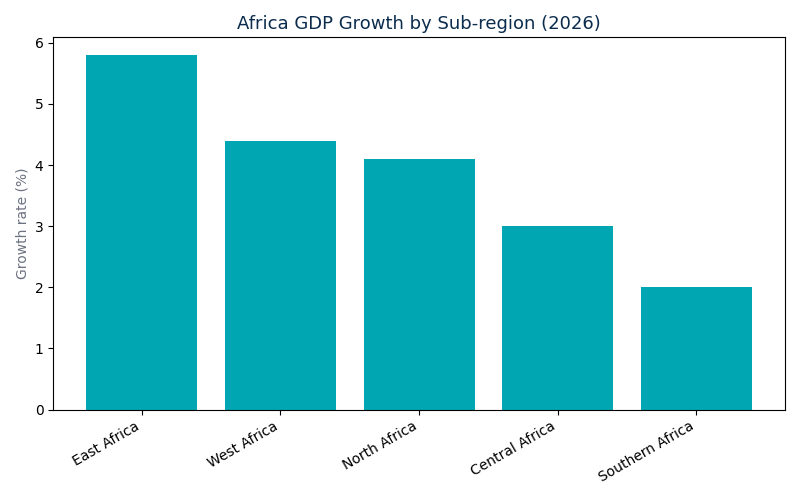

One of the most important features of the 2026 outlook is regional divergence.

According to the UN’s projections:

East Africa is expected to be the fastest-growing sub-region, with growth of around 5.8% in 2026, supported by infrastructure investment, services, and energy projects.

West Africa is forecast to grow by about 4.4%, driven by large domestic markets and improving conditions in key economies.

North Africa is projected at 4.1%, benefiting from recovery in tourism, manufacturing, and trade.

Central Africa is expected to grow by around 3.0%.

Southern Africa lags at approximately 2.0%, constrained by structural challenges and energy shortages.

For businesses and investors, this divergence matters.

Africa’s growth story in 2026 is not continental in a uniform sense but market-specific.

Decisions on expansion, capital allocation, and partnerships increasingly depend on choosing the right countries and sub-regions rather than adopting a broad “Africa strategy.”

While growth is improving, debt continues to weigh heavily on Africa’s economic outlook.

The UN estimates that Africa’s average public debt stands at around 63% of GDP, with interest payments consuming close to 15% of government revenue in many countries.

Around 40% of African countries are either already in debt distress or at high risk of falling into it.

This debt burden limits governments’ ability to invest in infrastructure, social services, and economic stimulus, areas that directly affect the business environment.

The World Bank reinforces this concern, noting that about 20 Sub-Saharan African countries are currently in, or close to, debt distress. Even as growth picks up, fiscal space remains tight.

For the private sector, this reality has practical implications:

Governments may reduce subsidies and increase taxes.

Public-sector payment delays may become more common.

Large state-led projects may face financing or implementation constraints.

In 2026, economic growth is occurring alongside fiscal restraint.

Another factor influencing Africa’s growth outlook is global trade uncertainty.

Rising protectionism, shifting tariff regimes, and questions around preferential access to major markets are already affecting African exporters.

In some cases, companies accelerated exports ahead of anticipated tariff changes, creating short-term gains that may not be sustained.

At the same time, progress on the African Continental Free Trade Area (AfCFTA) has been slower than initially expected.

While the agreement holds long-term promise, uneven implementation means that intra-African trade is not yet offsetting global volatility at scale.

For businesses operating across borders, this environment demands:

Greater flexibility in supply chains.

Diversification of export markets.

A stronger focus on regional African demand, not just Europe, the US, or Asia.

A quieter but significant shift affecting Africa’s 2026 outlook is the decline in official development assistance (ODA).

OECD data shows that global aid fell by 9% in 2024 and is projected to decline further by 9–17%, with Sub-Saharan Africa expected to face a 16–28% reduction in bilateral aid from major donors.

While aid is not the primary driver of private investment, it plays a stabilizing role in many economies – supporting healthcare, education, humanitarian response, and foreign-exchange availability.

As aid declines, governments may face additional pressure on budgets and social services, increasing the importance of private capital, blended finance, and sustainable commercial models.

Despite these challenges, Africa’s 4.0% growth outlook highlights clear areas of opportunity.

Energy and power remain central. Investments in renewables, grid stability, and power generation are critical to unlocking industrial growth and improving operating conditions for businesses.

Trade and logistics infrastructure—ports, transport corridors, warehousing, and digital trade systems will be increasingly important as companies adapt to shifting trade patterns.

Digital and financial infrastructure continues to offer strong potential. Platforms that reduce transaction costs, improve access to finance, and support SMEs are well positioned in a constrained but growing economy.

Above all, businesses that improve productivity and efficiency, helping governments and firms do more with limited resources, are likely to perform best.

Nairobi-based Purple Elephant Ventures (PEV), a startup studio focused on tourism, has secured an extra $500,000 to boost its seed funding round to $5 million.

Global impact investor Acumen has made a strategic investment in AgroEknor, a Nigerian agribusiness focused on the production, processing, and export of hibiscus.

Norfund, the Norwegian Investment Fund for Developing Countries, has announced its first-ever direct investments in plastic recycling initiatives in Africa