Uganda’s UTel to Receive $225 Million Investment from Rowad Capital

Uganda Telecommunications Corporation Limited (UTel) is poised to receive a significant financial boost with a $225 million investment from Rowad Capital Commercial (RCC) LLC.

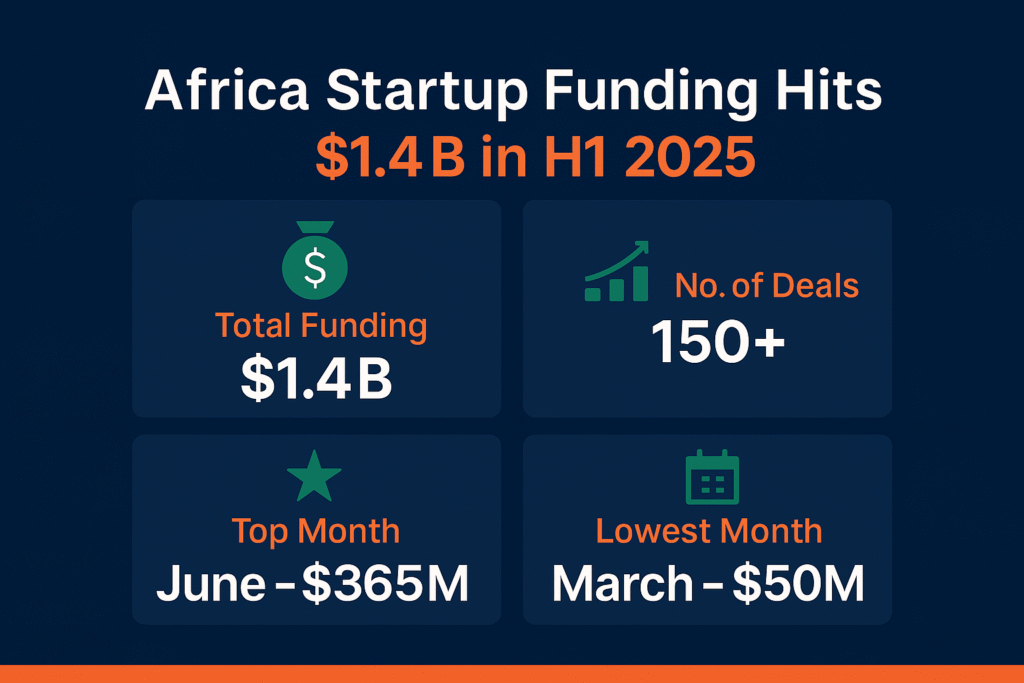

This marks a +78% increase compared to H1 2024, when just $800 million was raised, and represents a strong comeback from the funding slowdown seen in 2023 and early 2024.

With $365 million raised in June alone—the strongest monthly performance in almost a year—the continent’s startup ecosystem is not just rebounding but gaining renewed momentum.

Monthly fundraising crossed the $250M mark four times in H1, and the average monthly funding rose to $237M, significantly higher than 2024’s average of $187M and H1 2024’s $133M.

The year started off on a strong note, with African startups surpassing the $1 billion mark by the end of May—seven weeks ahead of the same milestone in 2024.

This makes 2025 the earliest $1B year since 2021, reinforcing the notion that Africa’s startup ecosystem is entering a new cycle of recovery and resilience.

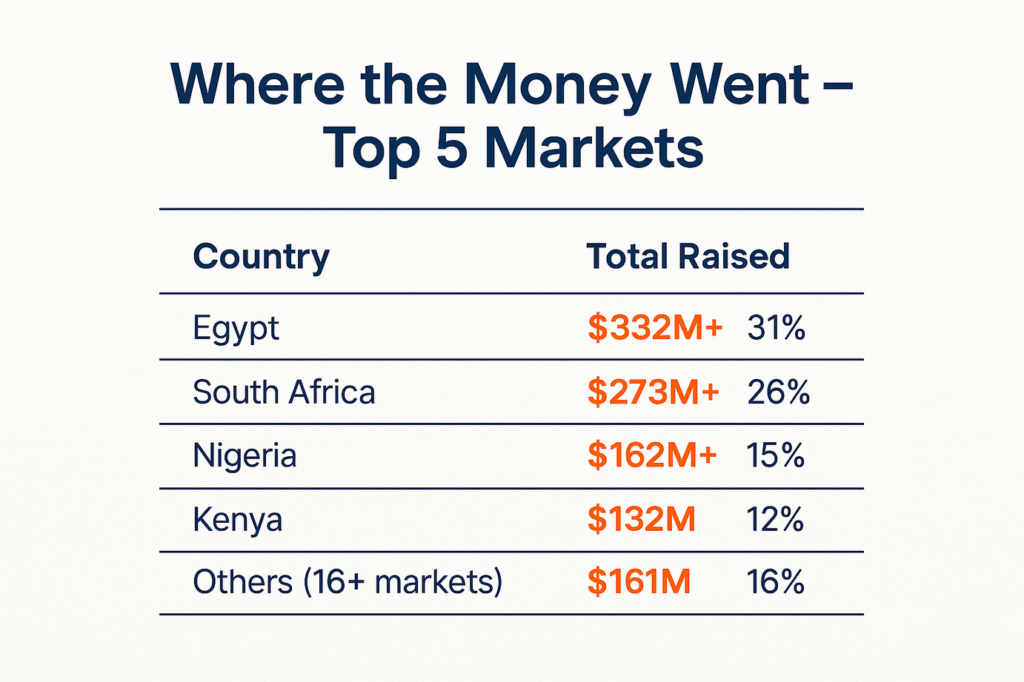

More than 20 African countries recorded deals above $100K between January and June, indicating a broader distribution of capital across the continent, not just in the usual hotspots like Nigeria, Kenya, Egypt, and South Africa.

Deals over $100K were recorded in 20+ countries, showing wider capital distribution across the continent.

Key Insights:

Six of the top 7 deals in May were from Egypt, highlighting its dominance this year.

On the equity side, startups raised $950 million in H1 2025—up 79% YoY, although slightly below H2 2024’s $1.02B (-7%).

However, debt funding stole the spotlight in June, contributing a whopping $227 million, including $137 million for Wave alone.

This pushed the total H1 debt funding to $400 million, a 55% increase from H1 2024 and nearly matching H2 2024’s performance.

This resurgence in debt brings non-dilutive capital back into focus for African startups, suggesting growing lender confidence and increasing maturity in venture debt markets.

P.S: While March 2025 saw a temporary dip in deal flow ($50M total), the sharp rebound in April ($343M) and continued strength in May ($254M) suggest that the lull was an anomaly, not a trend.

Uganda Telecommunications Corporation Limited (UTel) is poised to receive a significant financial boost with a $225 million investment from Rowad Capital Commercial (RCC) LLC.

South African artificial intelligence (AI) software company Spatialedge has secured R60 million (approximately $3.15 million USD) in funding from Hlayisani Growth Fund.

One Acre Fund, a social enterprise empowering smallholder farmers in East Africa, has secured a $1.4 million investment from Impact Bridge Asset Management.