Despite this, key sectors like transport, fintech, and cleantech continued to attract significant investments.

Kenya emerged as the leading country in startup funding, while Nigeria, South Africa, and Egypt remained critical players.

The increased reliance on debt financing and persistent gender disparity underscores the evolving dynamics and challenges within the African startup ecosystem.

These trends indicate a cautious yet sustained interest in key sectors, highlighting the resilience and adaptability of African startups amid global economic pressures.

Overall Funding Amounts:

Overall Funding Amounts:

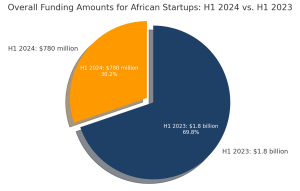

This indicates a significant decline of about 57% in total funding from H1 2023 to H1 2024.

The “Big Four” countries (Nigeria, Kenya, South Africa, and Egypt) continue to dominate, with Kenya emerging as the leader in H1 2024.

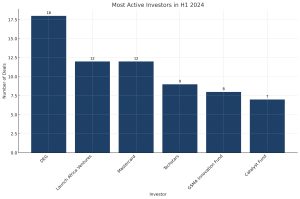

Most Active Investors:

In the first half of 2024, African startups raised a total of $780 million in funding, marking a significant decline compared to previous years.

This amount represents a 31% decrease from the second half of 2023 and a 57% drop from the first half of 2023.

Here is a breakdown of the funding by country and sector:

Despite the overall decrease, the “Big Four” countries—Nigeria, Kenya, South Africa, and Egypt—continued to dominate the funding landscape, attracting the majority of investments.

The distribution highlights the ongoing interest in sectors like transport and logistics, fintech, and energy.

The first half of 2024 experienced a significant reduction in total funding for African startups, with a 57% drop compared to the same period in 2023.

This decline is attributed to the challenging global economic environment, characterized by macroeconomic issues, tighter monetary policies, and higher interest rates.

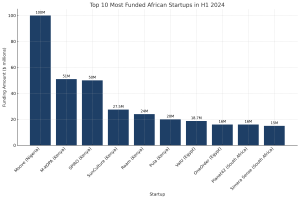

ANKA, an Ivorian SaaS e-commerce platform for African businesses, has raised $5 million in a pre-Series A extension round led by the International Finance Corporation (IFC) with participation from Proparco and Bpifrance.

d.light, a leading provider of solar-powered solutions, has secured $7.4 million in financing to advance their Pay-Go service and broaden access to solar products for low-income households in Nigeria.

German development finance institution DEG (Deutsche Investitions- und Entwicklungsgesellschaft) has confirmed it will commit $50 million to African Development Partners IV (ADP IV), the latest private equity vehicle managed by Development Partners International (DPI).